(Adobe Stock Image)

January 19, 2026

The home entertainment industry settled into a more stable pattern in 2025, with the free ad-supported streaming and transactional marketplaces complementing a subscription streaming business that began to rake in more profits and increase its dominance in Hollywood.

Streaming is expected to continue to flex its muscle in 2026, with Netflix on the verge of gobbling up Warner Bros. Discovery’s studio and streaming businesses — and with growth coming mostly from ad-supported models, along with live sports and other event programming.

The transactional business, meanwhile, will continue to serve as a premium monetization bridge between theatrical, subscription and free viewing — reinforcing ownership, catalog value, and event-driven releases in an otherwise flat-fee streaming world.

Looking back, much of what happened in 2025 set the stage for what is expected to happen in 2026.

Whether or not Netflix ends up jumping over political, regulatory and other hurdles in purchasing much of WBD, the top streamer has clearly won the streaming wars. Even before the studio buy, analyst Evan Shapiro stunned the audience at a NATPE session in Miami early in the year when he proclaimed that the streaming wars were over — and Netflix had won.

The analyst, who charts media’s future through his essays on his Media War & Peace Newsletter and co-hosts “The Media Odyssey” podcast, cited Netflix’s high subscriber count, which dwarfs that of the other subscription streaming heavyweights, and noted that the company’s valuation at the time was significantly higher than the combined valuation of Comcast, Disney, Fox, Paramount and Warner Bros. Discovery.

Shapiro now says he sees Netflix as the likely winner in the Warner battle, “but I do anticipate a dark horse to enter the race if Netflix hits bumps on the approval process.”

“Depending on when Tim Cook makes an exit, it could be Apple,” he posits, which would also be a streamer taking over a Hollywood studio.

Paramount Skydance still lurks, however, and could emerge triumphant in buying Warner Bros. Discovery, adding the studio’s HBO Max streaming service to its direct-to-consumer lineup, including Paramount+, led by former Netflix exec Cindy Holland.

“Regardless of whether Netflix or Paramount wins Warner, HBO is highly likely to see a greatly expanded reach and see accelerated growth,” says Wedbush Securities media analyst Michael Pachter. “Netflix is more likely to integrate HBO into its core offering, which will accelerate growth even more rapidly.”

In an added flourish to Netflix’s year, the service beat out Prime Video after three years at No. 2 on Parks Associates’ “Top 10 SVODs by Subscribers” chart.

Netflix’s financial footprint also dwarfed its competitors in 2025. For the year, Netflix delivered $45.2 billion in revenue, up 16% year over year. Ad revenue rose more than 250% to more than $1.5 billion. Net income for the year was $10.98 billion, versus $8.71 billion in 2024. Netflix ended 2025 with more than 325 million paid subscribers, up from 301 million subs at the end of 2024.

Disney’s direct-to-consumer business segment, which includes Disney+, Hulu, ESPN+ and the recently launched ESPN Unlimited, in September reported a fiscal-year profit of $1.3 billion, a massive increase from the $143 million the company reported for the prior fiscal year. Disney+ and Hulu (Hulu and Hulu + Live TV) together had 196 million paid subscribers worldwide as of Sept. 30.

Paramount’s direct-to-consumer segment, which includes Paramount+, Pluto TV and BET+, reported net income of $153 million for the year through Sept. 30, a reversal from a net loss of $211 million in the prior-year period. Paramount streamers ended the period with 79.1 million paid subscribers, up 10% from the previous year.

Warner Bros. Discovery’s direct-to-consumer segment reported a profit of $977 million through Sept. 30, up significantly from $268 million in the prior-year period. The segment, which includes HBO linear, HBO Max and Discovery+, reported 128 million paid subscribers, up from 110.5 million in 2024.

NBCUniversal’s Peacock streaming service was an outlier, reporting a net loss of $533 million for the year through Sept. 30. The platform ended the fiscal period with 41 million paid subscribers, up from 36 million subs a year earlier.

Apple TV ended its fiscal year (12 months ended Sept. 27) with a reported 45 million paid subscribers. The company does not break out direct-to-consumer fiscal data.

And Amazon’s Prime Video reportedly has more than 200 million subscribers across 23 countries. Amazon does not break out subscriber or fiscal data for the streaming platform, which is also available as a standalone service, and is included free with a Prime membership. Media reports suggest Prime Video generated revenue of $17.5 billion in 2025, up from $14 billion in 2024.

The pervasiveness of streaming is underscored by Parks Associates’ latest annual “State of Streaming” report, which found that the SVOD market as a whole has achieved a 91% penetration rate among U.S. households. The pay-TV business, in comparison, has a meager 41% household penetration rate.

On average, according to Parks Associates, U.S. SVOD households subscribed to 5.9 SVOD services in 2025, up from 5.6 in 2024. Parks Associates expects the average number of SVOD services subscribed to by SVOD households in 2026 to grow slightly, to 6, driven largely by bundling and discounted promotional rates.

As streaming became even more entrenched in U.S. homes, SVOD services felt safe to go on a price hike binge. Netflix kicked off 2025 by increasing prices for all U.S. plans, raising the ad-supported plan to $7.99, the standard ad-free plan to $17.99, and the premium plan to $24.99 monthly. Disney, HBO Max and Apple TV+ (now just Apple TV) subsequently raised their monthly subscription prices by a few dollars as well.

Streamers will continue to raise prices going forward, predicts Michael Goodman, director of entertainment research for Parks Associates. He says the price hikes, particularly on premium tiers, “are as much about driving consumers to the ad-supported tiers as they are about driving revenue growth.”

After falling 2.6% in 2025 to an average of $10.96 as cheaper ad-supported tiers took hold, average revenue per SVOD service will once again grow in 2026, Goodman predicts, reaching $11.30 by the end of the year.

“As to when we will see price hikes slow or even stop, it is largely in the hands of consumers,” Goodman maintains. “Until we see net adds stall or decline as a result of price hikes, services have no incentive to stop raising prices.”

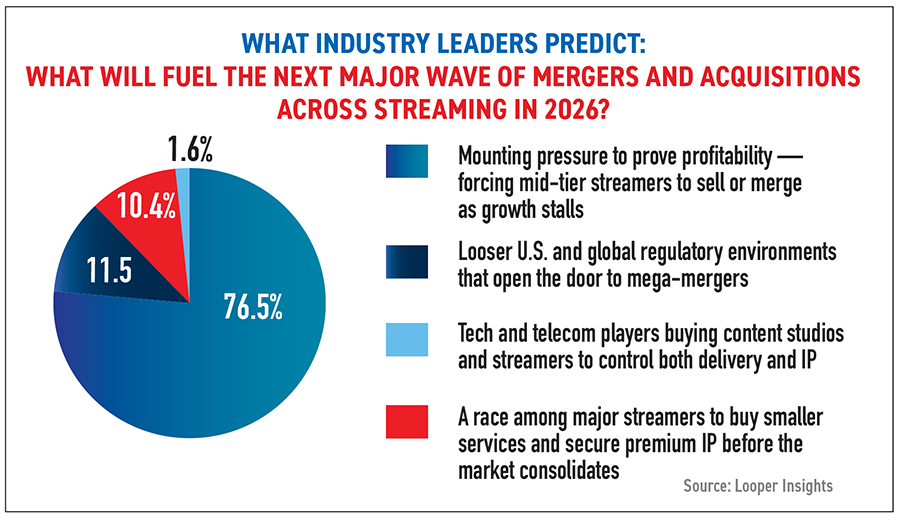

In a search for increased profits, the industry can also expect more consolidation in the coming year, according to industry leaders surveyed by Looper Insights. In the survey, a whopping 76.5% expect that mounting pressure to improve profitability will force mid-tier streamers to sell or merge as growth stalls. That consolidation will mean less new content for consumers.

“Streaming consolidation is likely to mean fewer shows overall, with budgets and attention concentrated on bigger, safer bets,” Parks’ Goodman says. “Mid-budget and niche originals are more likely to be cut, shows will be given less of a chance to prove themselves and will be canceled faster, and franchises, sequels and event programming that can travel globally and reduce churn will be prioritized.

“As ad-supported tiers grow, platforms will favor sticky content like procedurals, reality and comfort TV that drive long viewing sessions, while libraries become less permanent as titles rotate in and out for cost control. While there may be the occasional mega-hits, overall there will be less experimentation, fewer risk-taking projects, and less catalog stability for viewers.”

Bundles, as they did in 2025, will increase, as services that are raising prices look to offer more value for price-conscious consumers.

“Regardless of who wins the fight for WBD, the direction is the same — fewer giants controlling more premium IP, which will lead to more bundling and fewer standalone ‘must have’ alternatives,” Parks’ Goodman says. “Instead of subscribing to services individually, a growing segment of the population will buy a bundle of SVOD services, either through the services themselves, TV providers, or broadband/mobile bundles, as this helps mitigate price increases and reduce churn. On the live-TV side, expect to see more skinny/genre-specific bundles such as sports, news, entertainment, etc., similarly to what YouTube TV and Sling TV are doing.”

Sling TV offers mini-bundles that allow consumers to curate their content choices, including sports.

“Look for churn-reducing bundling across lifestyle products — especially from mobile and retail platforms,” analyst Shapiro adds.

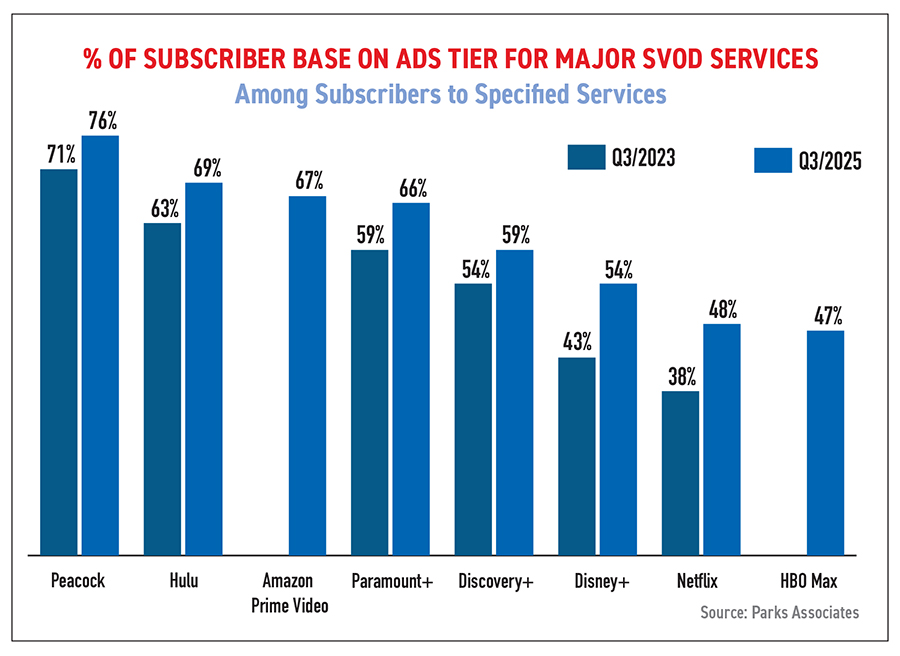

Another key trend that developed in 2025 and is expected to accelerate in 2026 is the expansion of ad-supported tiers to lower the price for subscribers. During the annual Tech Trends to Watch presentation Jan. 4 at this year’s CES in Las Vegas, show marketing and communications VP Melissa Harrison called out “the rise of ad-supported streaming” as a primary driver in a projected 4.2% uptick for 2026 in consumer spending on software and services.

“With 34% of subscribers to ad-supported tiers saying the lower monthly price makes SVOD services more affordable, and an additional 31% not minding ads if it saves them money, affordability is becoming a significant factor in SVOD subscription growth, while providing an alternative to cancellation,” Parks’ Goodman says.

According to the Parks Associates Subscription TV Forecast, ad-supported tiers are projected to account for all SVOD subscription growth in 2026, growing from nearly 363 million in the U.S. in 2025 to nearly 376 million in 2026. At the same time, subscriptions to ad-free premium tiers are projected to fall slightly from 280 million in 2025 to 279 million in 2026.

“Coinciding with this will be more features designed around ads (i.e., targeting, new formats), and in some cases increased ad loads,” Goodman says.

Analyst Shapiro is even more bullish on ad-supported free streaming.

“I predict that the ad-free TV viewer will disappear,” adds Shapiro. “Yes, viewers will have some ad-free experiences, but all regular TV viewers will see ads, every week, in sports, news, and through unavoidable ads on their TV home screen.”

The industry is entering a new era, pundits say, where, in many ways, streaming is television.

Lucas Bertrand, founder and CEO of Looper Insights, calls it a “reset phase.”

“The challenge in 2026 isn’t content volume anymore; it’s visibility,” he says. “As discovery shifts to TV operating systems and AI assistants, even the biggest streamers will have to work much harder to secure visibility.”

Consequently, in Looper Insights’ survey of industry leaders, the biggest segment (37.7%) said unified discovery across multiple streaming services and live channels will drive the next generation of streaming user interfaces in 2026.

Hub analyst Mark Loughney forecasts that Amazon will tackle the discovery problem.

“As frustration with content search and discovery reaches a tipping point, 2026 could see Amazon Prime Video introduce a universal video search experience that spans platforms — including services outside the Amazon ecosystem,” he predicts. “By positioning itself as the easiest place to find anything to watch, Amazon stands to become a default viewing hub.”

Subscribe HERE to the FREE Media Play News Daily Newsletter!

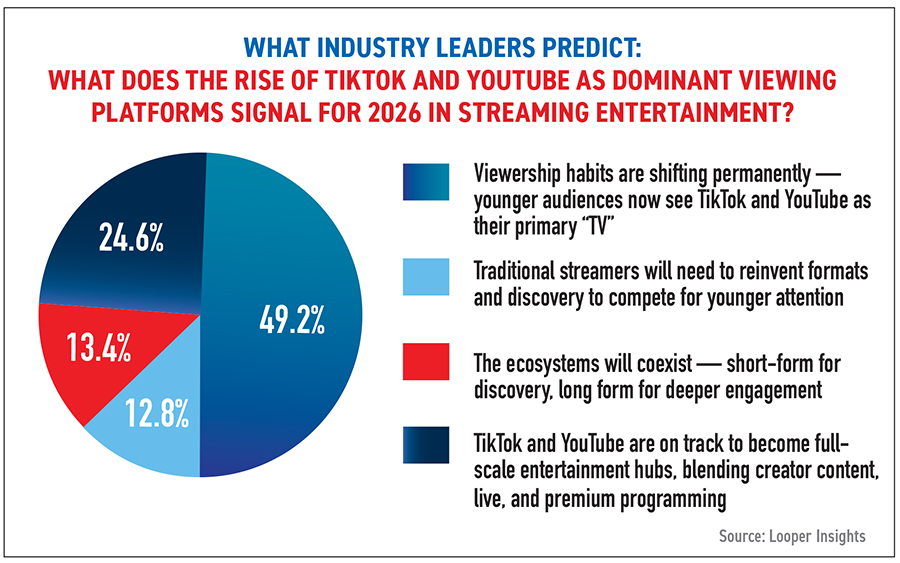

Looming large in the background of the streaming landscape is YouTube, the streaming behemoth owned by Google, which is ramping up the competition.

“Traditional streamers aren’t competing with each other anymore; they’re competing with YouTube for TV viewers’ attention,” Looper Insights’ Bertrand notes. “That means rethinking discovery, pacing, and even creator-driven formats if they want to stay relevant.”

“Next summer, on TVs, YouTube will surpass all of broadcast combined,” analyst Shapiro predicts.

The streaming goliath has already made inroads in the traditional TV space. YouTube got into the sports game in 2025, exclusively live-streaming the first game of the 2025 NFL season in São Paulo, Brazil, in September to a worldwide audience (outside North America) on YouTube and YouTube TV. This marked the first exclusive NFL game to be streamed live and for free in its entirety on YouTube. YouTube also tangled with Disney over carriage costs on its OTT pay-TV platform YouTube TV. The dustup left YouTube TV subscribers unable to watch content from Disney networks, including ESPN, ABC, Disney Channel, FX, National Geographic and Freeform.

The two companies ultimately settled their dispute, but the fracas showed YouTube was ready to go toe-to-toe with traditional media giants. As a coda to YouTube’s shift into the traditional TV space last year, the Academy of Motion Picture Arts and Sciences signed a multiyear deal giving YouTube exclusive global rights to the Oscars — a broadcast TV staple — from 2029 to 2033.

A key component to YouTube content, the independent creators who populate its service, will also move into the traditional entertainment space, many predict.

“The Affinity Economy — the melding of the Creator Economy and Traditional Media — will take over,” Shapiro says. “This means that more creators will become studios and more studios and brands will act like creators — leaning into social video and the rules of the Creator Economy.”

“Next year we’ll see creators bypass social platforms entirely and go straight to the living room via AVOD and FAST,” says Vikrant Mathur, co-founder of FAST channel distributor Future Today. “These streaming platforms are the new frontier as they’re more flexible, more aligned with how audiences actually watch content, and lucrative, opening new sustainable revenue streams for creators.

“This shift is already under way from the MrBeasts of the world, to other creators such as Like Nastya, Gemma Stafford, and more. With the wealth of audience data and insights CTV environments provide, advertisers can better align with creator-led content that reflects brand values and drives meaningful engagement.

“That’s the revolution: Brands finally have the precision to support creators who build genuine communities and deliver measurable results. The next wave will be long-form IP and creator-led channels that fill the cultural and emotional gaps traditional television left behind.”

The free ad-supported model that YouTube pioneered has become a fixture in the traditional content streaming marketplace.

As the FAST (free ad-supported streaming television) sector closed out 2025, one thing was clear: The category has moved decisively beyond its early “cord-cutter alternative” phase and into the core of the home-entertainment ecosystem. What was once viewed as a secondary distribution outlet is now a primary viewing destination for millions of households — and an increasingly important revenue lever for platforms, programmers and advertisers alike.

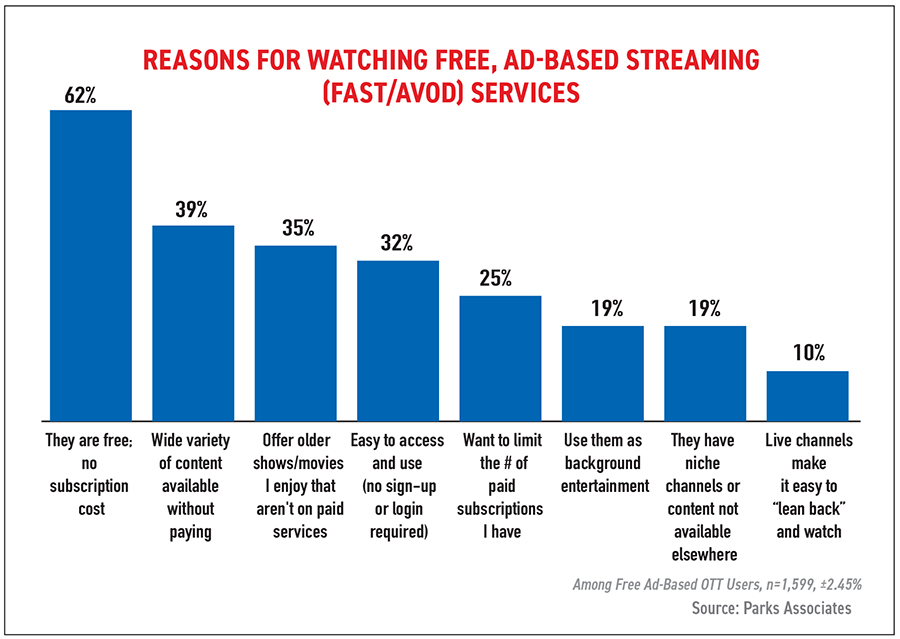

In a Looper Insights survey conducted in June 2025, nearly nine out of every 10 consumers said they’d rather watch ads on a free service than pay for a subscription with ads. More than one-third of consumer respondents said they watch more FAST content than they did a year ago, and 88% said they’re open to exploring free ad-supported channels. On the industry side, 83% of media execs said FAST is now central to their strategy, while 50% said they believe FAST is overcrowded or lacks standout content. FAST channels have proliferated in recent years. Gracenote, the content data business unit of Nielsen, found the number of FAST channels grew nearly 14% in 2025 through the end of July (and 76% since 2023).

“FAST has moved beyond being a free afterthought. In 2026 it’s becoming a premium, intentional part of the streaming mix, a core revenue driver and a critical front door into paid ecosystems,” says Looper Insights’ Bertrand.

“Free ad-supported streaming television (FAST) channels have emerged as a critical complement, offering a low-barrier entry point for consumers while generating new advertising revenue streams,” according to Parks Associates.

Observers say 2025 was something of a year of validation for FAST. Throughout the year, Media Play News tracked steady increases in viewing time, advertiser interest and strategic investment across major FAST platforms.

In a 2025 survey of more than 8,000 domestic broadband households, Parks Associates found that consumers’ use of free ad-based services had doubled over the past six years, from 23% in the first quarter of 2023 to 46% in the third quarter of 2025. Nearly two-thirds of respondents in the Parks study said that the fact that FAST/AVOD services were free was their top reason for tuning in.

One of the most important developments in 2025 was FAST’s deeper integration into the broader streaming ecosystem. Rather than existing as standalone destinations, FAST increasingly became embedded within larger platforms and operating systems. Amazon’s move to fold Freevee’s free programming into Prime Video, and the growing prominence of FAST hubs on smart-TV home screens, underscored a shift toward aggregation and discovery over app sprawl. Indeed, Chinese TV manufacturer Hisense, via backend technology from Xumo, joined consumer electronics giants such as Vizio, LG, Samsung and TCL in offering a branded FAST service in August 2025.

The marketplace also experienced a growing maturity in how FAST content was programmed. The emphasis in 2025 shifted away from rapid channel proliferation toward recognizable brands, franchises and libraries that drive repeat viewing.

David Di Lorenzo, SVP of kids and family for Future Today, says 2026 will bring FAST consolidation without contraction.

“The FAST space is slated to mature as the days of launching a ‘whatever we can license’ channel are over,” he says. “In 2026, volume for volume’s sake is out; editorial vision, thematic cohesion and audience intention are in. Viewers are no longer grazing — they’re looking for streaming with a point of view. Expect a rise in creator-led channels, lifestyle verticals, and brand-aligned experiences that feel more like destinations than dumping grounds. Live content, especially news and sports, will show up more in FAST, but not as standalone plays. It will come wrapped in the infrastructure of trusted AVOD platforms where distribution, data and audience already live. That’s the difference between launching a channel and launching an ecosystem. The winners will be the platforms and partners who know their audience, stay disciplined, and build with long-term resonance — not short-term trend-chasing.”

“The next phase of FAST growth is about quality and moments, not just channels,” Looper Insights’ Bertrand adds. “Live events and sports are turning FAST into a frontline viewing experience for audiences.”

Indeed, in 2025, free ad-supported service Tubi made history simulcasting the Super Bowl with Fox Sports. The simulcast saw a record-setting average audience of 127.7 million viewers and generated more than $800 million in gross revenue from ads.

It’s expected that 2026 will see increased interest in growing ad profits.

“We are going to see a lot of the same as we saw for streaming entertainment platforms in 2025, but intensified to focus on increasing profits, while challenged by an increasingly crowded ad space,” says Keith Valory, CEO of free ad-supported service Plex. “It’s important to be conscious of the consumer’s mindset in this high-pressure economy. Interest in and usage of freemium services like Plex is only going to increase. It’ll make for a ripe space for advertisers to get creative, and we are focused on maximizing their creativity with premium ad bundles that can endemically reach the consumer on many surfaces of our platform.”

On the business side, measurement and credibility became central themes in 2025.

Advertisers pushed for more-consistent metrics, improved frequency management, and better alignment with traditional TV-buying expectations.

In the June 2025 Looper Insights survey, 64% of viewers rated FAST as a “good or great value,” but 50% of executives cited inconsistent ad tech and measurement as the most significant barriers to monetization. Viewers were showing up, but the dollars were getting stuck in the funnel, according to Looper Insights.

As a result, FAST platforms spent much of the year tightening ad tech, refining data partnerships, and positioning themselves as reliable, brand-safe environments rather than opportunistic remnant inventory.

Artificial intelligence will come to the rescue in smoothing the bumps in ad tech, Future Today’s Mathur predicts, flipping the power dynamic in advertising within the next year.

“Small and mid-sized businesses will compete on the same playing field as the world’s biggest brands — not because they’re spending more, but because they’re thinking smarter,” he says. “The same sophistication that once required big budgets and agency-scale resources can now be achieved through intuitive, AI-powered platforms. The next wave of AI innovation will be less about flashy creative tools and more intelligence at the infrastructure level: real-time price floor optimization, dynamic audience segmentation, and contextual tracking that works without IDs or cookies.”

Looking ahead in 2026, FAST is expected to enter a phase of disciplined optimization.

Growth will continue, but it will be more intentional. Channel lineups are likely to slim down, not expand, with underperforming channels quietly sunsetting and stronger brands receiving better promotion and placement. The success metric will no longer be the sheer number of channels launched, but the efficiency with which platforms monetize viewer attention.

FAST’s role as a top-of-funnel engine should also become more explicit in 2026. Studios and rights holders are expected to use FAST strategically to extend the life of IP, reintroduce franchises, and funnel viewers toward premium SVOD tiers, transactional rentals and physical media releases.

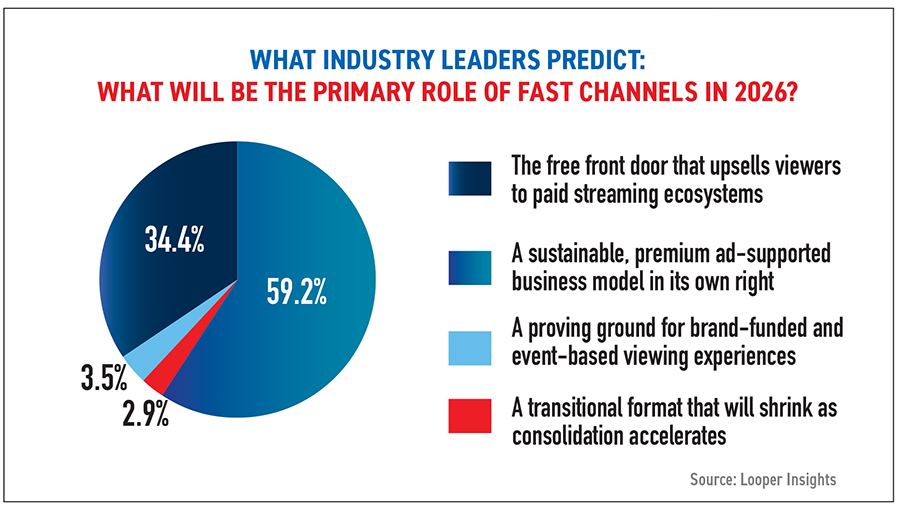

In the Looper Insights survey of industry leaders about how they see FAST’s role taking shape in 2026, more than half (59.2%) said that FAST will become a sustainable, premium ad-supported model in its own right. Meanwhile, one-third (34.4%) said that FAST would be a free front door that upsells views to paid streaming ecosystems. Only 2.9% said FAST is a transitional format that will shrink.

“The industry now views this space as a core revenue driver — not simply a side channel, but a meaningful pillar of the wider streaming economy,” the report concluded.

A major merger of indies in 2025 underscored the durability of free ad-supported streaming as New York-based FAST/AVOD powerhouse FilmRise was combined with Los Angeles-based Shout! Studios, also a major FAST channel supplier. Owner Oaktree Capital changed the name of the combined company to Radial Entertainment and appointed as CEO former Paramount streaming executive Jeff Shultz, who cut his teeth at free ad-supported streaming powerhouse Pluto TV.

“The FAST ecosystem is maturing from an experimental phase into a core pillar of the global content economy,” says David Buoymaster, chief investment officer and chief content officer at Radial Entertainment. “As audiences fragment and platforms look to distinguish themselves in an increasingly crowded and competitive marketplace, we’re seeing a flight to quality — both in programming and in how platforms curate and monetize the user experience. The next wave of winners in FAST won’t just be those with the most channels, but those that can align premium libraries, smart data, and differentiated brand identities to capture sustained viewer engagement.”

Heading into 2026, FAST will look even more like “TV,” not less — with improved program guides, tighter ad loads, and packaging that appeals directly to traditional TV advertisers seeking scale without the cost structure of legacy linear, observers say.

The transactional market — including digital and physical — has become a small part of the home entertainment ecosystem, but in 2026 it is expected to sharpen its role as a premium revenue channel and a strategic bridge in the release window ecosystem.

Top titles often follow a clear progression: theatrical, premium-priced then lower-priced digital purchase and rental, (sometimes) physical disc, SVOD and eventually free ad-supported models (FAST/AVOD). In this model, transactional acts as the monetization bridge, ensuring that studios capture revenue before content is absorbed into flat-fee or free ad-supported environments.

Indeed, for the year of 2025 through September, revenue for digital purchases grew a solid 4.34% to $1.75 billion, according to data from DEG: The Digital Entertainment Group.

A 2025 Parks Associates survey found that 15% of consumers had bought or rented a movie via a connected-TV platform in the prior 30 days. Meanwhile, 6% bought or rented TV episodes.

Collecting titles digitally is lining up as a cost-effective entertainment option, particularly with the rising price of subscription services, says Cameron Douglas, SVP of OTT/streaming for Fandango, who heads up the company’s video-on-demand streaming service Fandango at Home, one of the industry’s leading digital retailers in the transactional space. Fandango is part of the new Comcast spinoff company Versant.

“We remain positive about the long-term viability of this category, particularly as consumers are becoming increasingly thoughtful about their digital entertainment spending habits, where as an example so much of the growth in subscription is now coming in the lower, ad-supported tiers,” he says.

“[Traditional, transactional] home entertainment remains an important part of our ecosystem, especially in the living room,” says Jonathan Zepp, managing director of entertainment content and platforms at Google, which offers digital sales and rentals of titles through its Google Play/YouTube marketplaces.

“Looking ahead, we’re optimistic about the transactional business,” says Adam Frank, EVP of global partner management, sales and distribution for the Lionsgate Motion Picture Group. “With industry forecasts projecting box office growth in 2026, we expect a corresponding lift in transactional home entertainment driven by new-release conversion. Lionsgate expects to be a meaningful contributor with two major event films — Michael and The Hunger Games: Sunrise on the Reaping — along with continued momentum from our 2025 holiday breakout The Housemaid and a diverse slate across action, thriller and horror.”

Lionsgate is already preparing a Housemaid sequel, based on the second novel in Freida McFadden’s best-selling trilogy, The Housemaid’s Secret, with plans for star Sydney Sweeney to return.

“Digital remains the strongest driver of transactional performance across our global business, underscored by robust consumer interest and the industry’s embrace of high-value experiences, which are transforming the transactional landscape,” says Justin Che, president of Universal Pictures Home Entertainment. “As we move through 2026, event-driven releases and major franchises — such as Steven Spielberg’s highly anticipated Disclosure Day, Christopher Nolan’s The Odyssey, and Illumination’s The Super Mario Bros. Galaxy Movie — along with Universal’s vast portfolio of catalog titles, will play a pivotal role in attracting new consumers and driving sustainable growth.”

Indeed, catalog is an enticement for digital collectors.

“One stat that keeps surprising us is the massive growth of catalog TV,” Douglas says. “You have your ongoing important business of whatever the hot new series is at the time, whether it’s ‘Game of Thrones,’ ‘Walking Dead,’ ‘Yellowstone,’ etc. But, even with FAST channels out there dedicated to single series like ‘Murder She Wrote’ or procedurals, we still see a massive interest in classic TV and full-series digital sets.”

“Catalog performance remains a key opportunity,” Frank says. “The category continues to show strength despite increased SVOD and AVOD engagement, as consumers still see strong value in owning films, particularly in 4K, for instant access and the ability to build a personalized library. Catalog titles also play an important role in customer acquisition, bringing new transactors into the digital ecosystem at rates comparable to new releases.”

It wasn’t all smooth sailing in the digital transactional segment in 2025. The Microsoft Movies & TV Store left the business, and, for a time, Google Play/YouTube left the digital rights locker service Movies Anywhere during a carriage dispute between YouTube TV and Disney (which runs Movies Anywhere, which allows consumers to buy an eligible title from any participating retailer and watch it through the site or another participating retailer). Online chatter mused about the continued viability of collecting content digitally. But as the year closed, Disney and YouTube TV patched up the relationship, and Google Play/YouTube returned to Movies Anywhere, preserving stability in the digital transactional marketplace.

Meanwhile, revenue on physical disc purchases, the legacy transactional industry, continued its slow decline in 2025, dropping 9.21% through September to $605.1 million, according to data from the DEG. Still, the sector is bolstered by collectors that are eager to snap up the 4K Ultra HD Blu-ray format and premium Steelbooks, the DEG reports.

Things are looking up for the physical disc business, according to Eddie Cunningham, president of Studio Distribution Services, which was established in April 2021 to distribute physical media from joint venture partners Universal Pictures and Warner Bros. Discovery.

“It’s been an incredibly exciting year for the physical business,” he says. “Clearly, the business trajectory is leveling out compared to what many had predicted. I think consumers are increasingly realizing the comparative benefits of packaged media, from having the best-quality picture and sound, through to the security of ownership for life. We are also beginning to see physical content becoming fashionable again with some younger consumers, and we know what happened with vinyl, so perhaps we can build on that.”

Like the DEG, he points to the growth of 4K UHD sales (up 16% for catalog, and up 28% for new releases) and Steelbook sales (up 10%) as major drivers.

“Catalog sales, at least for SDS, are close to flat year-on-year for our two owners, something that was unimaginable just a few years back,” he notes.

E-commerce (up 15%) continues to fuel some of the success, both through the traditional retailers and the Gruv brand, an online shop run by Universal Pictures, he reports.

Indeed, after several years of retreat, retail participation is stabilizing, Cunningham says.

“Our retail partners have continued to lean into the category with effective holiday promotions,” he says. “Walmart expanded its promotional space in 2025, while Best Buy re-entered the category online through its third-party marketplace, quickly driving incremental sales with added promotional placement.”

“We’re also committed to serving physical media collectors through Lionsgate Limited, our direct-to-consumer storefront for curated specialty releases,” says Lionsgate’s Frank.

“Demand has exceeded expectations, and in just over a year we’ve sold out multiple titles, including Kill Bill Vol. 1 and Vol. 2, Apocalypse Now — Final Cut, Basic Instinct and most recently the long-awaited 4K release of Dogma.”

The physical disc continues to attract movie and TV content connoisseurs, Cunningham maintains.

“Collectability remains important,” he says.

Collections and new-to-format releases — including first-time 4K UHD and Steelbook editions — continue to fuel demand among collectors, he says. Key 2025 catalog Steelbook releases included James Bond 007: Sean Connery 6-Film Collection, The Dark Knight Trilogy, Kingdom of Heaven, Tombstone, Master and Commander: The Far Side of the World and Superman 1978-1987 5-Film Collection, he says. Franchise and collection releases remained top performers as well, he says, led by “The Lord of the Rings,” “Venom,” “Harry Potter,” and “Jurassic World.” Television franchises also performed strongly, with “Yellowstone,” “Supernatural” and “Game of Thrones” ranking among the year’s top disc sellers.

Like consumer enthusiasts, the industry remains aware of the key attractions of physical media — including its tangible qualities.

“From a marketing perspective, studios and retailers increasingly recognize that franchise awareness, combined with compelling artwork, premium packaging and exclusive extras, is critical to the physical consumer, clearly differentiating physical media from digital and streaming experiences,” he says.

Additional reporting by Thomas K. Arnold and Erik Gruenwedel